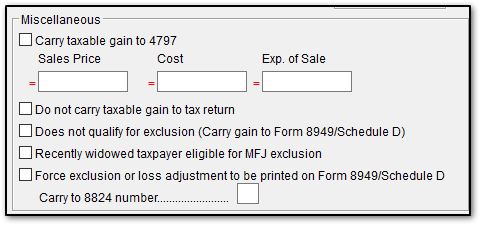

Not known Details About Home Sale Exclusion: Intro to IRC Section 121 - 1031Gateway

The Facts About Base Year Value Transfer Age 55+ - Assessor - Marin County Uncovered

Nevertheless, post-May 6, 1997 depreciation allowed on nonresidential usage can set off gain acknowledgment on the residential-use part of your home. Leann used 10% of her home as a workplace for a service. She owned and utilized the house as a principal home for at least two years throughout the five-year period prior to she offered it.

On January 1, 1999, Morton purchased a home that he used partly for company functions. Learn More Here sells the house on January 1, 2002 having actually owned and used it for three years. Morton realizes a $40,000 gain on the sale, of which $30,000 is attributable to the domestic portion of the home and $10,000 to business portion.

The gain on the domestic portion of the house eligible for exclusion ($30,000) is decreased by $2,000 the amount by which the depreciation deductions go beyond the gain on the business-use portion of the home ($12,000 devaluation minus $10,000 gain). For that reason, Morton will leave out $28,000 ($30,000 minus $2,000) from earnings but will include $12,000.

The 4-Minute Rule for Estate tax

However, if Morton had taken devaluation reductions of $7,000, the gain on the residential portion of the home eligible for exclusion ($30,000) would not be lowered because Morton's devaluation deductions ($7,000) did not go beyond the gain on the business-use part of the house ($10,000). Therefore, he would exclude $30,000 from income however consist of $10,000.

Taxpayers who jointly own a principal house, however file different returns, might each omit approximately $250,000 of the gain attributable to their interest in the house. An other half and partner who submit a joint return might leave out up to $500,000 of the gain if Either spouse satisfies the two-year ownership requirement.

Neither spouse left out gain from a prior sale or exchange of a principal home within the last 2 years. If the taxpayers do not fulfill any one of these requirements, the optimal exemption amount a married couple can declare on a joint return is the sum of each partner's exemption quantity, determined as though (1) the spouses were not married and (2) each spouse owned the home throughout the duration that either spouse owned the home.

Public Last updated: 2022-03-20 08:44:18 AM