A Complete Guide to Understanding Your True Home Loan Value

Understanding the actual amount of your mortgage is a critical step in the real estate acquisition process. Many first-time purchasers focus primarily on the cost of the home or the monthly payments, frequently overlooking other essential factors that can significantly impact their financial obligations. By comprehending your true mortgage amount, you can make knowledgeable decisions that correspond to your budget and long-term economic aims.

In this guide, we will walk you through the process to correctly calculate your actual mortgage. From principal and interest rate to property taxes and insurance costs, each component contributes to your overall monetary commitment. Using a mortgage calculator can streamline this process and help you gain a clearer picture of what to expect before you sign a loan. By the conclusion, you will feel more empowered about your mortgage process.

Grasping Home Loan Estimators

Home loan estimators are essential instruments that simplify the process of figuring out how much you can manage to borrow for a house. By inputting various variables such as loan amount, interest rate, and loan term, these calculators generate estimates for monthly mortgage payments. This can help aspiring homeowners assess their budget and grasp the financial commitment involved in buying a house.

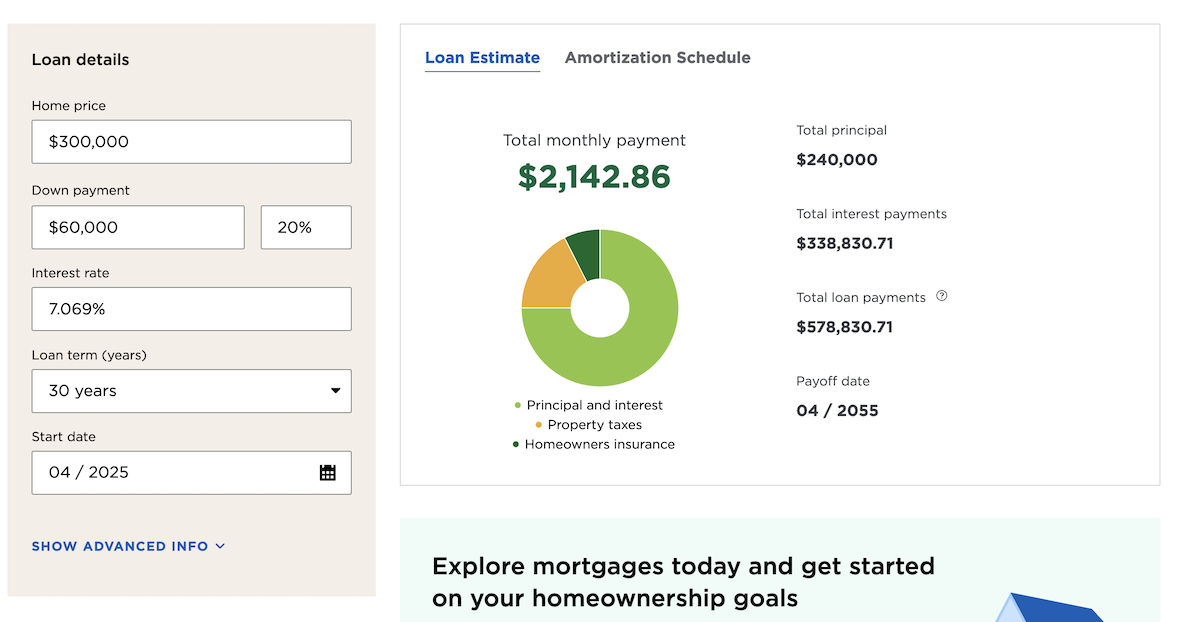

Using a mortgage calculator usually requires entering essential information, including the loan amount you are evaluating, the rate rate presented by financial institutions, and the length of the loan. Many calculators also account for supplemental costs such as real estate taxes, home insurance, and private mortgage insurance. By examining these factors, you can get a clearer picture of your financial standing and potential monthly payments.

Moreover, mortgage calculators can help in exploring alternative scenarios. For example, you can change the loan amount or interest rate to see how it affects your monthly cost. This feature is particularly advantageous for new owners who may need to test with various figures to find a pleasant financial strategy. With this knowledge, you can form educated decisions that match with your future financial objectives.

Calculating The True Mortgage Total

To determine your true mortgage amount, start by gathering all pertinent monetary information. It includes the sale cost of the home, the initial payment, and any fees that may apply. A down payment is typically a percentage of the home price, commonly varying from 3 to 20 %, based on the loan type. Closing fees can differ greatly, so it’s important to get a good faith estimate from the mortgage provider to include these into the overall cost.

Once you have this information, you can use a loan calculator to enter these figures. Input the property cost, initial payment, and other significant details like interest rates and loan terms. The calculator will help you understand how various factors affect your monthly payment and the overall mortgage amount you are assuming. Such knowledge is vital for understanding the financial commitment and assists you steer clear of overextending the finances.

Finally, remember to account for extra expenses that are associated with owning a home, such as taxes on property, home insurance, and costs of upkeep. Such expenses can add substantially to the overall monthly spending. By including these elements into the calculation, you will obtain a clearer understanding of your actual mortgage amount and what you can realistically manage.

Factors Influencing Mortgage Calculations

When determining your true mortgage amount, several factors must be considered that can substantially impact the final numbers. First and foremost, the interest rate you secure holds a crucial role in determining your monthly payments and overall loan cost. A lower interest rate can result in substantial savings over the life of the loan, while even a slight increase can boost your payments and total interest paid. It's important to compare rates from multiple lenders and understand how factors such as your credit score affect what you can qualify for.

Another key factor is the loan term. Mortgage loans typically exist in multiple lengths, with the most common being 15 or 30 years. A longer loan term generally leads to lower monthly payments, but it also means paying more interest over time. Shorter loan terms may have higher monthly payments but can save you money on interest in the long run. Depending on hipotecalc.com and long-term goals, choosing the right term can significantly affect your mortgage calculation.

Lastly, your down payment amount significantly influences your mortgage calculation. A larger down payment reduces the loan amount you need to borrow, which results in lower monthly payments and reduces the total interest paid over the life of the loan. Additionally, putting down at least twenty percent can help you avoid private mortgage insurance, which adds another layer of cost. Understanding how your down payment impacts your overall mortgage can enable you to make informed decisions as you navigate the buying process.

Public Last updated: 2025-08-01 05:57:17 PM