Decoding Mortgages: A Comprehensive Calculation Guide

Understanding home loans often can seem like navigating a maze, with intricate terms and numerous figures that appear intimidating. Many potential buyers often discover themselves asking, what’s true loan cost? This question is essential, yet difficult to respond to without the right tools. Thankfully, a mortgage calculator is able to simplify this procedure, offering insight on how loans, interest rates, and other factors add up to your total financing.

In this guide, we will break down the steps necessary to calculate your actual mortgage, making sure you are prepared to make informed financial decisions. From comprehending principal and interest to including taxes and insurance, we will demystify each aspect of the mortgage calculation. By the end, you will not only know how to use a mortgage calculator but also be confident in grasping the true cost of your loan. Let us embark on this path toward financial literacy together.

Understanding Home Loan Basics

A mortgage is a financial agreement exclusively used to purchase real estate. It requires taking on money from a lender, commonly a financial entity or lending organization, that must be paid back with finance charges over a specified time frame. The property purchased acts as security, meaning if the homebuyer fails to make installments, the lender can reclaim the property through repossession.

When evaluating a home loan, it's important to understand critical concepts such as loan amount, interest, and duration. The principal is the amount borrowed, while finance charges is the expense of borrowing that principal. The length refers to the period of time you have to pay back the loan, which usually ranges from 15 to thirty annual periods. A longer duration generally results in lower installments but higher finance charges accrued over the life of the financial obligation.

Home loan installments typically consist of both loan amount and finance charges, and might also comprise additional costs such as property taxes, homeowner's insurance, and PMI. To assist prospective homebuyers assess cost-effectiveness, many utilize a loan calculator, which provides a rapid calculation of installments based on the principal, finance rate, and duration. Understanding these basics will allow you to make wise choices when selecting a mortgage.

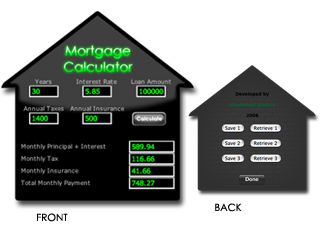

How to Use a Mortgage Calculator

Utilizing a mortgage calculator might make easier the complicated process of figuring out your monthly payments. Start by inputting the home price, which is the total you intend to borrow. Numerous calculators typically ask for your down payment proportion, which lowers the total amount financed. By inputting these figures, you can get a clearer picture of your loan amount.

Next, type in the interest rate and loan term. The interest rate affects how much you pay over the life of the loan, so it's essential to apply an correct rate based on your credit score and market conditions. The loan term, typically spanning from 15 to 30 years, will also affect your monthly payment and the total interest paid over time. This information will help you understand the overall costs associated with your mortgage.

Once entering all relevant data, the calculator produces an estimate of your monthly payment, including principal and interest. Several calculators also offer insights into property taxes, insurance, and any private mortgage insurance that may apply. This holistic view can aid in budgeting and figuring out a specific mortgage fits your financial situation.

Deciphering Your Findings

When you have submitted all the necessary data into your mortgage calculator and received your results, it's crucial to take a moment to interpret what those numbers indicate. The calculator will typically provide you with your regular payment amount, which includes both principal and interest. However, you may also see projections for property taxes, homeowner's insurance, and possibly private mortgage insurance if your down payment is less than 20 percent. Understanding these elements is key for gaining a complete picture of your periodic financial responsibility.

Then, consider the total cost you'll pay over the duration of the loan. This number can often be alarming, as homeowners may realize that they end up paying significantly more than the initial loan amount due to interest accumulation over time. Pay attention to how different loan terms, such as 15 years against 30 years, can significantly affect this total cost. Shorter terms typically mean increased monthly payments but lower total interest paid, while longer terms offer lower payments but can lead to considerably more overall interest.

Finally, reflect on how your computed mortgage fits into your overall financial scenario. hipotecalc.com to see how the suggested monthly payment aligns with your income and additional expenses. It's important to ensure that you can comfortably handle the mortgage payments along with other financial obligations. This comprehensive view will help you make thoughtful decisions about the suitability of the mortgage for your personal circumstances.

Public Last updated: 2025-08-01 06:35:43 PM