What Does Business Basic Obligation Cgl Insurance Policy Cover?

What Does & Doesn't Business General Responsibility Insurance Policy Cover?

Along with business basic responsibility plans, companies might also buy policies that supply protection for other business dangers. In the UK we have a tendency to call it 'service liability insurance policy' or 'public and item responsibility'. Your cover level is the maximum amount that your insurance company will certainly pay out if you make a claim.

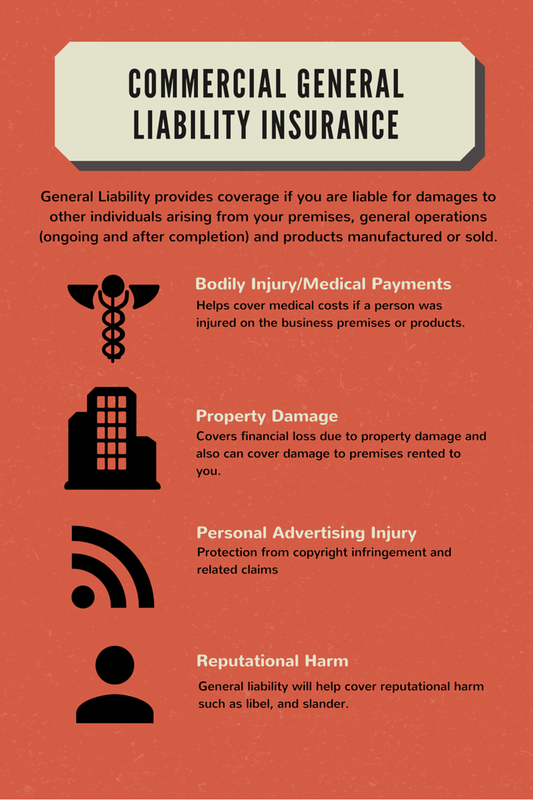

Commercial basic responsibility insurance policy, typically described as CGL insurance coverage, is a form of commercial insurance coverage that covers your company against third-party claims for physical injury or residential property damages. These claims can develop from the use of your service or products, and likewise cover circumstances where you may have caused physical injuries or property damages. Finishing up and obtaining ideal basic responsibility insurance policy coverage uses indispensable benefits tiny firms require to properly handle integral service dangers.

Specialist Civil Liability

Likewise, if you would certainly battle to work without your specialised devices, then tool insurance will keep those covered against theft and damages.Conditions are provisions that detail the responsibilities and obligations of the insured and the insurance company.TechInsurance helps small company proprietors compare service insurance policy prices quote with one very easy on the internet application.You can also secure the contents of your business premises, your service tools and devices.Product responsibility insurance coverage shields your company from third-party claims associated with items you make or sell.

Markel's insurance services can help a wide range of small companies, consisting of individual instructors, clinical offices, service providers, eateries, in-home child care and much more. The conditions of the insurance coverages explained are laid out in the insurance policy, which always dominates. The company that authorized the agreement with the client might not be the one primarily responsible for the damages. As an example, if a building professional subcontracts the electrical job and the subcontractor triggers damage to the building, the building professional might be held liable.

As an entrepreneur, you deal with daily dangers that might lead to crashes or injuries taking place on or around your business properties. But basic responsibility has its constraints-- usually you buy Claims Management limits of $1,000,000 or $2,000,000 per incident which might be insufficient in the event of a major insurance claim. That's why I advise that company owner take into consideration purchasing excess liability or umbrella obligation protection along with their basic responsibility insurance coverage. Product responsibility insurance policy provides protection for cases related to damages or injuries caused by items your organization produces, distributes, or offers. It's particularly crucial for companies that deal with physical items, such as makers, dealers, and retailers. Specialist liability insurance, additionally called errors and noninclusions insurance, covers claims of carelessness or failing to supply ample expert services or advice.

How Much Residential Or Commercial Property And Responsibility Insurance Policy Is Enough For Your Business?

The price of business liability insurance policy coverage versus the impact of taking care of the economic influence of a case suggests public responsibility insurance coverage can make all the distinction for lots of services. Public responsibility insurance coverage (as general liability is understood in the UK) supplies cover for public injury and damages claims. It can likewise cover a variety of other responsibility insurance policy items consisting of companies' liability and item liability. In the UK, public obligation insurance coverage and product responsibility insurance coverage offers to protect organizations from these claims and the prospective financial losses as a result. Entrepreneur are exposed to a variety of liabilities, any of which can subject their properties to considerable insurance claims. All local business owner require to have an asset defense plan in place that's built around offered obligation insurance coverage.

Expected/intended Injury Exemption

Moreover, if you're not sure regarding plan protection, make sure to talk to your insurer-- they will be able to explain what is or isn't covered under your policy. No entity operates without vulnerabilities, so this organization insurance policy and proprietor's plan insurance policy reinforces continuity ability. Maintaining company insurance policy and owner's insurance plan enhanced via routine options like elevating limitations, adding new Commercial vehicle liability supplementary security, or altering insurance providers helps danger management initiatives. With wise assistance from an expert broker, all companies can access monetary security and guarding to focus on lasting development.

Some of the usual exemptions include injuries to employees and willful damages brought on by the business. As an entrepreneur, it is very important to understand the risks you deal with on a daily basis. From slips and is up to building damage, mishaps can take place at any time, leaving you susceptible to considerable financial losses. That's why it's vital to have basic obligation insurance policy coverage in position. A policy may include properties protection, which safeguards business from claims that happen on the business's physical area during routine company operations.

Public Last updated: 2024-12-28 07:45:51 PM